Colliers report warns aged care occupancy nearing 100%

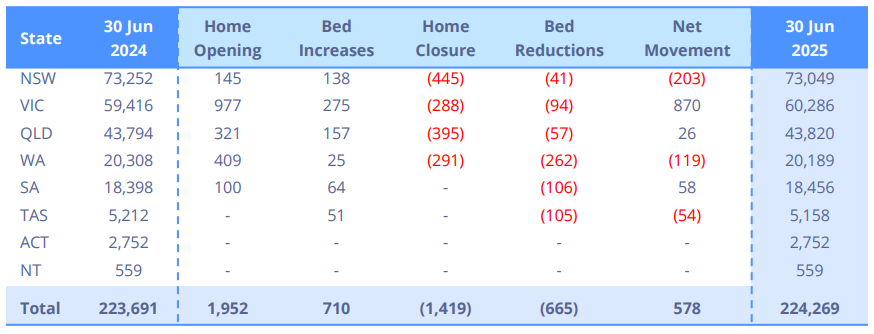

Collliers new Residential Aged Care Market Report, compiled by Boxwell & Co’s Darren Lynch, reveals the sector added only 578 new residential aged care places in FY25.

Australia’s residential aged care sector is rapidly approaching full capacity.

New data shows the number of operational beds grew by just a fraction last financial year as demand surged ahead.

The new Residential Aged Care Market Report, released by Colliers and compiled by Boxwell & Co’s Darren Lynch, reveals the sector added only 578 new residential aged care places in FY25, far below the projected increase in demand of more than 9,000 residents.

That 578 figure is even lower than the 800 net new beds previously identified in Colliers' analysis of the 2025 Aged Care Service List, after Boxwell & Co queried and adjusted the underlying Departmental data.

In total, 21 new homes opened nationwide over the period – delivering 1,952 new beds – while 20 homes, representing 1,419 beds, closed – see below.

Private operators continued to lead development activity, accounting for 64% of new beds, with much of the delivery coming from groups such as Arcare and For Purpose. Just two new projects benefited from Federal capital grants, underlining the limited reach of current capital programs.

‘No vacancy’ sign looms for sector

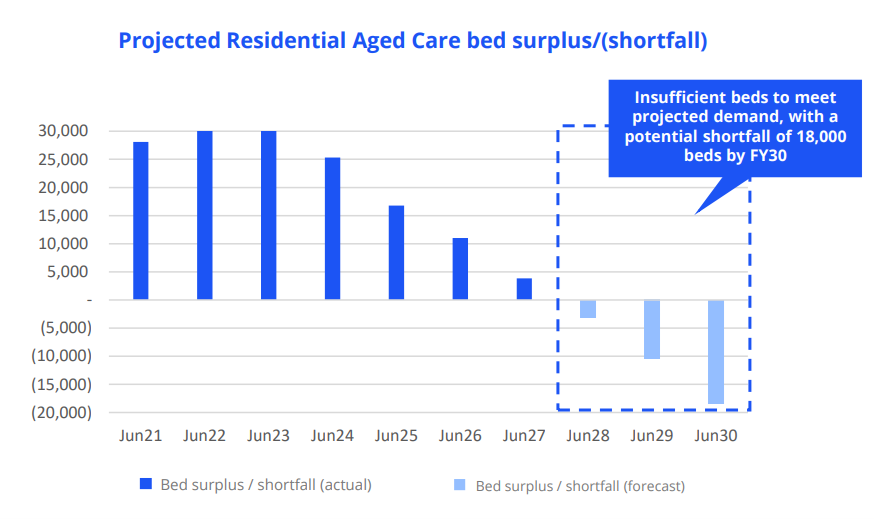

The national average occupancy now stands at 94.4%, and Colliers forecasts the sector will reach a theoretical 100% by FY28 – or closer to FY27 in practice, once offline rooms are taken into account.

Some regions are already experiencing no immediate availability, with residents who have complex care needs, behavioural challenges or limited means most likely to be turned away.

“This is not a provider behaviour issue; it’s a funding issue,” said Darren. “Government responses have been incremental and politically driven rather than strategic. It takes four to five years to deliver a new home – the time for decisive action is now.”

The report projects an 18,000-bed shortfall by FY30, warning that without structural reform, the imbalance will worsen and flow directly into public hospital demand.

Immediate action

With the economics of new development increasingly marginal for both Not For Profit and private operators, the Colliers-Boxwell report sets out five immediate recommendations to restore investment confidence and accelerate supply:

- Increase the Accommodation Supplement now, without waiting for the Government’s Accommodation Review;

- Allow providers to lift RAD retention to 4% per annum – double the current 2% retention rate;

- Simplify HELF arrangements to give developers revenue certainty;

- Reinstate payroll tax supplements for new homes; and

- Ensure care margins are explicitly built into future AN-ACC funding.

“The economics simply don’t support development at scale,” said Ian Sanders, Colliers Head of Transaction Services, APAC Healthcare & Retirement Living.

“If Government wants private capital to step up, it must create an investable environment – and quickly.”