Residential aged care still falls short on investability: EBITDA $6.8K vs $20K target

Residential aged care remains well below investable thresholds, according to StewartBrown’s FY25 survey, which puts average EBITDA at $6,817 per bed per annum (pbpa) a long way off the $20,000-$22,000 the firm says is needed to attract ongoing capital and deliver enough new beds for the Baby...

Residential aged care remains well below investable thresholds, according to StewartBrown’s FY25 survey, which puts average EBITDA at $6,817 per bed per annum (pbpa) a long way off the $20,000-$22,000 the firm says is needed to attract ongoing capital and deliver enough new beds for the Baby Boomer wave.

Earnings are heading the wrong way too: EBITDA fell 3% from $7,039 last year.

StewartBrown forecasts EBITDA could lift to $13,406 by FY30, depending on reform settings, but that would still miss the investability mark.

The downgrade reflects the recently announced AN-ACC starting price and changes to the Net Weighted Activity Unit (NWAU). On FY25 survey data, 27.5% of permanent residents are set to receive a higher NWAU under the Government’s AN-ACC decision, while 69.5% will see a decrease.

Care margins erode

Providers recorded an average operating deficit of $3.10 per bed day (pbd), nearly double FY24’s $1.58 pbd shortfall. Losses deepened in everyday living services (to -$7.13 pbd from -$5.61 pbd) and accommodation services (to -$12.05 pbd from -$11.22 pbd). Direct care – traditionally used to cross-subsidise those losses – also weakened.

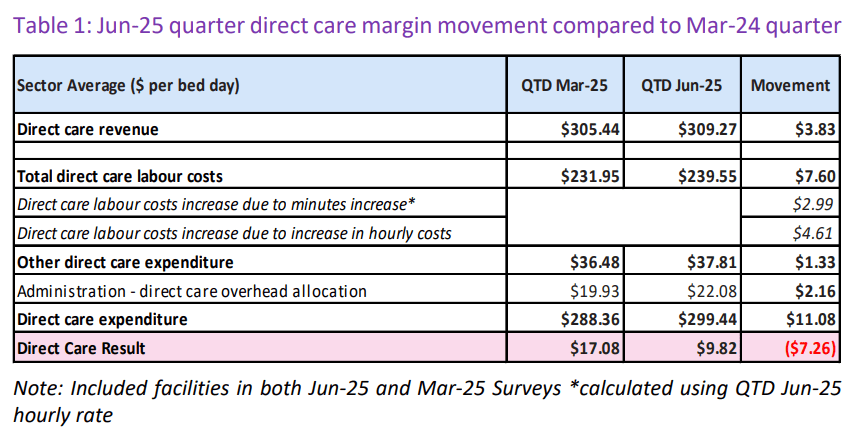

While the AN-ACC (direct care) margin ticked up across the year to $16.07 pbd (from $15.25 pbd), it fell $2.39 pbd in the June FY25 quarter as providers lifted direct care minutes ahead of penalties for missing mandatory targets. StewartBrown expects further erosion in FY26.

Bed squeeze intensifies

Average occupancy rose to 94.4% (from 92.6% in FY24), reflecting stronger demand against stagnant new bed construction over the past 4-5 years. StewartBrown anticipates occupancy above 95% across the coming decade.

The FY25 survey draws on responses from around 1,200 residential aged care homes, accounting for roughly half the sector.

For our analysis of StewartBrown's home care results click here. You can read the StewartBrown report in full here.