Aged care funding likely to need to increase 50% to 100%: Aged Care Royal Commission releases consultation paper on financing – and calls for submissions

You can download the paper on the Commission website here

A social insurance scheme – similar to the Japanese model – an aged care levy, personal donations and even keeping the current system are among a range of options being canvassed by the Royal Commission in its latest consultation paper. You can download the paper on the Commission website here. So, what are the options being outlined in the paper?

- Keeping the current taxpayer-funded system with co-contributions

- Introducing an aged care levy similar to the Medicare Levy

- Increasing co-contributions by refining means testing and asset testing arrangements

- Developing a social insurance model with mandatory contributions

- Creating a public or private aged care contributory scheme

- The use of a private aged care insurance scheme

- Lump sum annuities

- Private gap insurance

- Tax deductions for long-term investments in aged care

- Individual donations

- A combination of the above options

See my longer analysis and information on how to make a submission below. Beginning with a quote from its first Adelaide hearing in February 2019 from COTA Australia CEO Ian Yates that “we need to have a conversation with the Australian people about what we’re doing with aged care”, the 54-page paper outlines how aged care is currently funded in Australia and overseas, and considers a range of options that have the potential to transform the way aged care is funded and delivered in Australia. The Royal Commission’s Interim Report – released last October – had argued the aged care system in Australia required “fundamental reform” – and would need a “significant injection” of funding to achieve this reform. Under the current aged care funding arrangements, around 75% of funding comes from the Commonwealth with consumers chipping in the remainder. But as the Royal Commission’s research has found, aged care spending in Australia only equates to about 1% of GDP – much lower when compared to other countries with comparable populations. Noting that aged care spending is already forecast to grow to 5.4% of Government expenditure in 10 years’ time – and Counsel Assisting’s recommendation for more services to help older Australians age at home – the Commissioners say they are working off the base that aged care expenditure will need to increase by between 50% and 100% (they add that this does not mean this will be their final recommendation, but is intended to give an idea of the funding challenges). The Commissioners also acknowledge the tough question: should people provide for their own care or should each generation pay for their elders? They add that while a pay-as-you-go system is simpler, it depends on a larger taxpayer base which is rapidly shrinking in Australia. A pre-funded system would be more complex and require a changeover period in which some people would be both contributing to their own aged care costs and paying for the previous generation. The Commissioners then go on to look at a number of options which fit under three broad approaches:

Minimal change

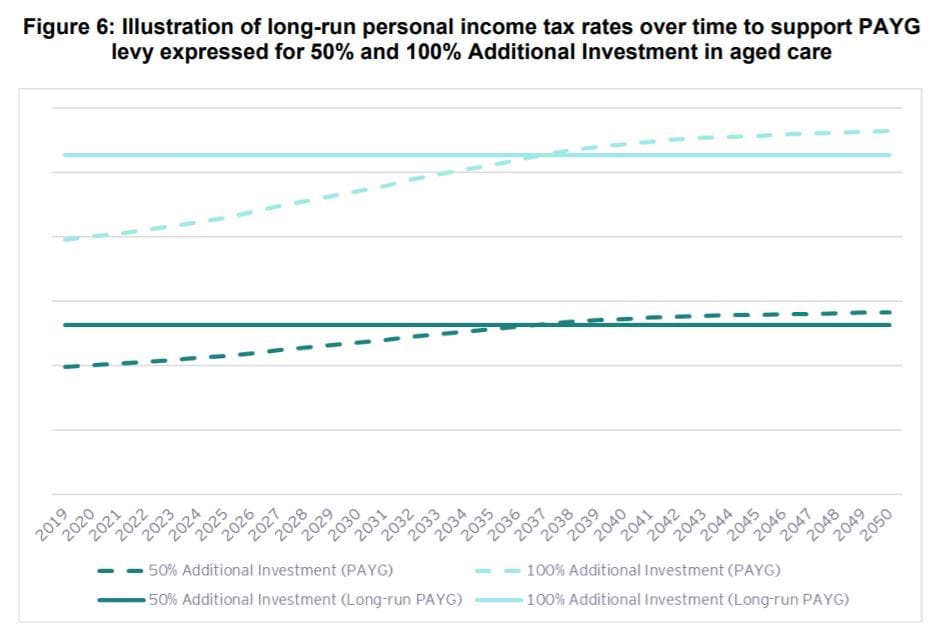

This option is based on continuing the current system taxpayer-funded aged care with co-contributions from users. The Commissioners say this approach has funded the system for the past 60 years and could work into the future, but say there is potential for aged care to be funded by an earmarked levy like the Medicare levy. These levies can be hypothecated – paid into a dedicated Consolidated Revenue fund which would only be for aged care and rolled over year to year – or non-hypothecated – where the funds are available to be spent on other purposes (again similar to the Medicare levy) (the NDIS is funded by a mix). To make sure the funds were only used for aged care, the levy would need to be hypothecated, the Commissioners state. However, it would come at a cost – to increase aged care funding by 50% would require a 1% increase in personal income tax rates, the paper says. A 100% increase would need a 2% rise. Despite home care recipients paying an average of $30 a week towards their care and aged care residents contributing an average of $502 a week (excluding RADs), the Commissioners also say there is scope to increase co-contributions by refining the existing means testing and assets testing arrangements – including for the CHSP.

Social insurance models

Noting this idea was considered by the Productivity Commission in its landmark 2011 report, the Commissioners say they see potential in a social insurance model where Australians would make mandatory personal contributions to pooled funds managed by either an Aged Care Insurance Commission or by private providers. A hypothecated pre-funded levy could also be another form of social insurance, they add, using the example of applying a levy to the incomes of people aged 25 to 65.

However, they acknowledge there would be a risk that the funds may not fully cover the costs of care at a given period, requiring the Government to top up funds. The paper also raised the idea of a public aged care contributory scheme, similar to the long-term compulsory social insurance scheme in Japan, where all Australians aged 25 to 65 for example would contribute and could be pay-as-you-go or pre-funded. Here, the Commissioners say there would need to be considerable planning, regulation and cost controls put in place, with potential oversight required by either an independent body or within the Department of Health. A private aged care contributory scheme is also flagged as an option with people given the choice of a range of private insurers (similar to the way Compulsory Third Party insurance operates), which would likely need to be pre-funded. The Commissioners add that while this could stimulate innovation in the delivery of aged care services, it could also raise risks for consumers and the Government.

Private insurance and other voluntary arrangements

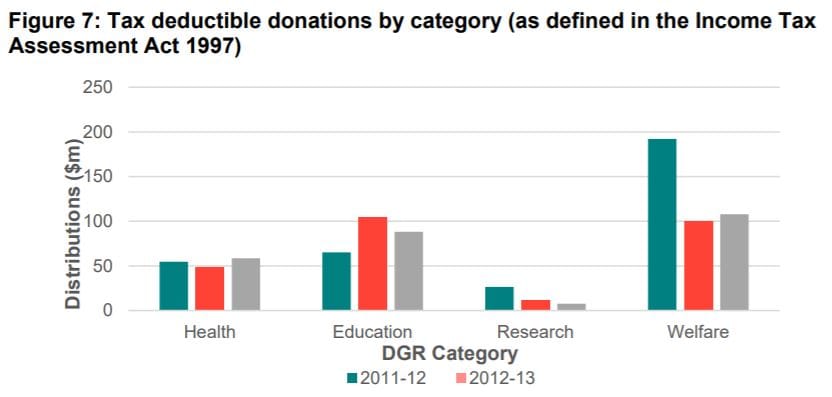

Finally, the paper examines the option of a private aged care insurance scheme and products (which make up just 0.9% of aged care funding across the OECD). The paper says the model could offer a viable alternative, but would need large numbers of people to take up the product to allow pooling and risk sharing. Lump sum annuities to pay for aged care costs, private gap insurance to cover extra aged care expenses and tax deductions for long-term investments in aged care (like school building funds) and even individual donations are also canvassed. The paper also acknowledges there is the potential to combine these options, for example, higher income tax plus a social insurance scheme, higher co-contributions and donations.

These could be used to fund care and accommodation separately, for instance, nursing and allied health supports through taxation and co-contributions while board or accommodation is personally funded. The Commissioners conclude that implementing any new financial arrangements would be “complex”.

“There will be a range of views on the questions we pose in this paper, and there will not always be simple solutions. This is, however, an important debate, and we encourage the Australian community to engage in this conversation in the interests of improving the quality and safety of care for older Australians.”

They will have their chance. Submissions on the ideas outlined in the paper are now open until close of business on Tuesday, 4 August 2020 – and could have a major impact on the Royal Commission’s Final Report.

“Subject to the responses we receive, it is our intention to consider a smaller set of options in more detail and undertake further modelling to inform the recommendations we make in our Final Report,” the Commissioners said in a statement.

You can email submissions to FinanceOptions@royalcommission.gov.au.