What is the cost of fragmentation amongst retirement village operators? We can calculate lost sales of $936 million and lost development profit of $140 million in 2018.

How do we come to this conclusion?

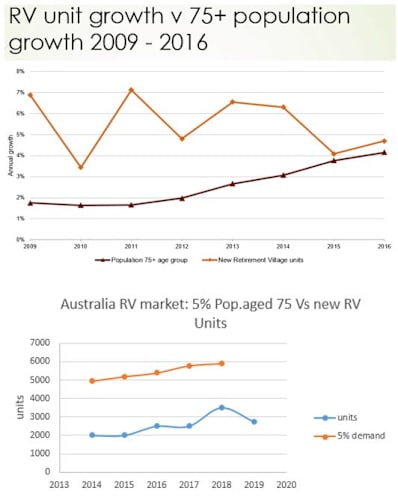

Check the top graph above which was presented by John Collyns, CEO of the NZ Retirement Village Residents Association, at our LEADERS SUMMIT 10 days ago. The top line shows the annual growth in new retirement village units built and sold each year in NZ; the growth ranges from 4.5% to 7%.

The bottom line shows growth in the population 75+ which is now up to 4% in 2016. They are building and selling faster than the market is growing.

The NZ retirement village sector is very tight. All but a very few operators belong to the peak body, John’s RVA. That is roughly 295 operators out of 300.

Here in Australia approximately 90 operators out of 600 belong to the Retirement Living Council, representing approximately 55,000 of 150,000 village units across the country. This is a fragmented sector.

The NZ village sector has been very successful in building the basic structures with consumers, investors and government for a mature industry. Think code of conduct, accreditation, trust and constant sales.

In Australia we don’t have any of these – yet.

And the impact for us is declining penetration (or ‘participation’). Few people have the confidence of the New Zealanders. The customers are there but not forcing down the gate to buy. And operators are not pushing to build significantly more.

Utilising our villages.com.au National Resident Survey from January, we can approximate today’s village customer as being aged 75, 35% singles and 65% couples.

The bottom graph shows the increasing population/market (target penetration of 5% of people turning 75) compared to the number of units being built.

In summary, every year back to the GFC we have been at least 40% short in building the number of village units we need to achieve 5% penetration.

2018 will be our best year yet with new stock – estimated as high as 3,500 new units built and sold. But the target should have been 5,889.

We are short 2,339 units which at an average sale price of $400,000 equals $936 million in sales and $140 million development profit (at 15%).

Over the past five years we have missed the market by 13,653 units – call that 136 villages. That is $5.46 billion in sales and $819 million development profit missed.

And the challenge is in 2019 new units are forecast to drop from 3,500 to 3,000 for the year.

Who or what is taking up the lost volume? Answer: staying at home, home care, apartments and technology.

The sector has a choice: become increasingly marginalised and ultimately irrelevant or follow NZ by investing in the fundamentals of building a strong, cohesive sector behind one peak body, which needs to be Retirement Living Council.