Bain Capital: why aged care operator looks attractive to buy

A 26-page IPO presentation has revealed the latest financial results for Australia’s second-largest aged care operator, with earnings boosted by efficiencies and the acquisition of 24 new homes.

The document has been prepared for fund managers as US-based Bain Capital pitches a sale or re-listing of Estia Health.

Since Bain swept Estia Health off the ASX at the end of 2023, a lot has changed in aged care. The sector has undergone significant consolidation, aged care staff have been granted Government-funded pay increases of more than 30%, and the new Aged Care Act has been implemented.

These factors are reflected in the results.

Estia reported revenue of $1.3 billion in the year to 31 December 2025, according to reports in The Australian Financial Review, up 71% on the $765 million posted in the 2023 financial year.

Earnings Before Interest Tax and Depreciation (EBITDA) climbed to $176 million, up more than 50% from $116 million in 2023.

The earnings growth was driven primarily by the addition of 24 homes over the more than two-year period, increased accommodation prices, and the centralisation of admin and procurement.

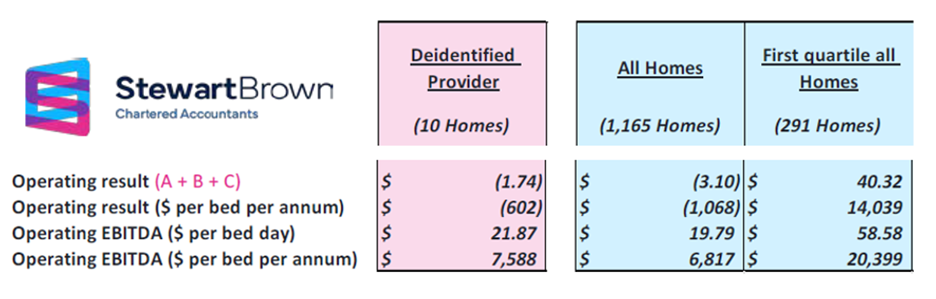

StewartBrown rates a top tier operator EBITDA return at $20,399 per bed. Based on a new acquisition cost of $300,000 per bed, this is a return of 6.8%, very desirable in a closed market where demand is growing against very little new supply.