KPMG: Top 25 home care providers hold share as market fragments

The top 25 home care providers account for 40.5% of total funding, according to KPMG’s 2026 Aged Care Market Analysis – a share that has stabilised after several years of decline.

Australian Unity has retained the top spot with $720.9 million in Government funding and a 7.3% market share, followed by Trilogy Care Pty Ltd with $340.01 million and a 3.4% share.

See the top 25 home care providers listed below.

Click to view

| FY23 Rank | FY24 Rank | FY25 Rank | Change | Provider |

|---|---|---|---|---|

| 2 | 1 | 1 | 0 | Australian Unity |

| 7 | 3 | 2 | ▲ 1 | Trilogy Care Pty Ltd |

| 3 | 2 | 3 | ▼ -1 | UnitingCare QLD |

| 4 | 4 | 4 | 0 | Home Instead Senior Care Group |

| 5 | 5 | 5 | 0 | Silver Chain Group |

| 14 | 8 | 6 | ▲ 2 | Dementia Caring Australia |

| 8 | 7 | 7 | 0 | Bolton Clarke |

| 9 | 9 | 8 | ▲ 1 | BaptistCare |

| 6 | 6 | 9 | ▼ -3 | HammondCare |

| 16 | 12 | 10 | ▲ 2 | Right at Home Group |

| 11 | 10 | 11 | ▼ -1 | The Uniting Church in Australia Property Trust (Victoria) |

| 32 | 17 | 12 | ▲ 5 | Self Managed Support |

| 10 | 11 | 13 | ▼ -2 | The Uniting Church in Australia Property Trust (NSW) + Wesley Community Services Limited |

| 15 | 16 | 14 | ▲ 2 | Resthaven Inc |

| 19 | 15 | 15 | 0 | FiveGoodFriends |

| 13 | 14 | 16 | ▼ -2 | The Corporation of the Synod of the Diocese of Brisbane |

| 12 | 13 | 17 | ▼ -4 | Baptcare |

| 29 | 22 | 18 | ▲ 4 | Pearl Home Care |

| 18 | 20 | 19 | ▲ 1 | Ozcare |

| 21 | 19 | 20 | ▼ -1 | ECH Inc |

| 17 | 18 | 21 | ▼ -3 | KinCare Health Services |

| 20 | 21 | 22 | ▼ -1 | Mercy Aged and Community Care |

| 26 | 23 | 23 | 0 | Just Better Care Australia Group |

| 27 | 26 | 24 | ▲ 2 | Suncare Community Services |

| 23 | 24 | 25 | ▼ -1 | Catholic Healthcare Limited |

But while the leaders remain relatively steady, the broader market is becoming more fragmented, according to the 18-page report released today (19 March).

The number of providers has grown to 873, up from 818 in FY18, with 14 new providers entering the market in FY25.

Many of these entrants are coming from the NDIS and adjacent health services, bringing new operating models and increasing competition.

Despite this expansion, funding remains concentrated at the top end.

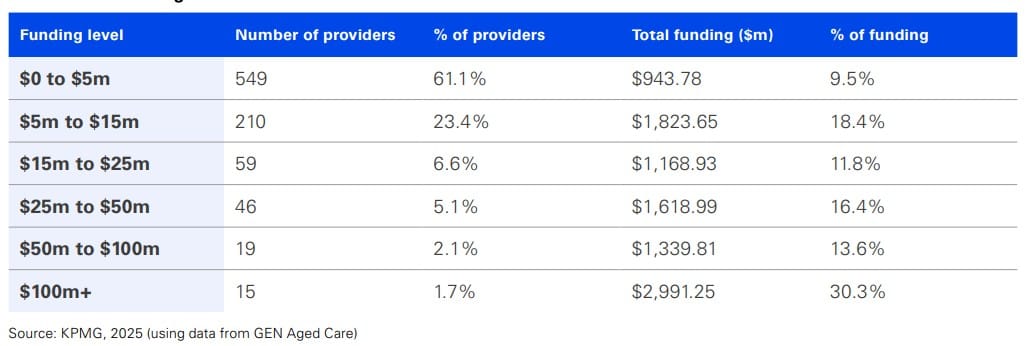

Just 15 providers – around 1.7% of the market – control more than 30% of total funding, while 61.1% of providers receive less than $5 million, accounting for under 10% of funding. See below.

At the same time, new models – including Trilogy Care and Self Managed Support’s self-managed approach – are gaining traction.

KPMG expects Support at Home to trigger further change, with smaller providers potentially exiting, mid-sized operators focusing on organic growth, and larger providers pursuing scale through acquisitions.

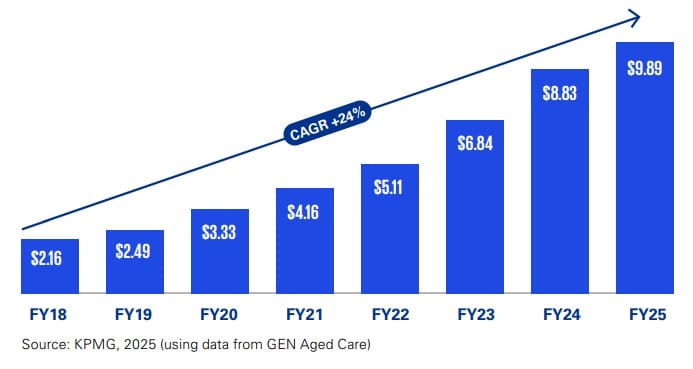

With an additional $1.1 billion in funding flowing to providers in FY25, investor interest is also tipped to increase.

“We are seeing significant renewed investor appetite for in-home aged care businesses from existing players in the sector, as well as private equity funds, as the implementation of the Support at Home reforms has provided clarity on the pricing and funding model,” Helen Sutherland, Partner, Aged Care M&A Specialist at KPMG Australia, said.

“Home care providers with a strong technology backbone, high-quality clinical governance and workforce compliance are attracting premium valuations.”

Read this week’s edition of SATURDAY, out tomorrow (20 March), for our interview with Lauren Ffrost, the report’s co-author and KPMG Director, Health, Ageing & Human Services, and further analysis. Not a subscriber? Click here.

You can download the KPMG report here.