Regis takeover bid sees sector-wide upgrade of aged care stocks – aged care can still be a profitable business if providers scale up

Last week’s news that Soul Pattinson had launched a bid for the listed provider has seen the share price of its rivals Japara and Estia upgraded – and shows that despite the impact of the Royal Commission and COVID, the sector can still pull in...

Last week’s news that Soul Pattinson had launched a bid for the listed provider has seen the share price of its rivals Japara and Estia upgraded – and shows that despite the impact of the Royal Commission and COVID, the sector can still pull in investors – as long as operators have the size to manage their costs. As we reported here in The Daily RESOURCE, Regis’ board rejected a $1.85 a share offer for the provider – valuing the company at $555 million – by conglomerate Washington H. Soul Pattinson and Regis co-founder Bryan Dorman on Friday. This followed an earlier bid on 30 September at $1.65 a share made by Soul Pattinson and Skip Capital – a private investment fund headed by Scott Farquhar, the co-founder of tech giant Atlassian. The takeover bid saw Regis’ share price rise to $1.79 after the offer with Japara and Estia also jumping 23% and 17% respectively. Regis’ board turned down the offer, saying it undervalued Regis and didn’t take into account what might come out of the findings of the Royal Commission’s Final Report on 26 February 2021 and the May Budget where the Government is expected to increase funding to the sector. But while the bid was rejected, Regis has set up an independent board committee and appointed Flagstaff Partners and Herbert Smith Freehills as advisers – indicating there is more to come.

Brokers revised listed players to ‘buy’

The brokers certainly believe so, with JP Morgan upgrading its recommendation on Japara and Estia to “overweight” (or “buy”).

“While the recommendations and the resulting Govt policy and funding decisions are uncertain we believe it is reasonable to assume FY21 will be a low point,” they said. “We believe investors should consider building a position in the sector now despite the continuing uncertainty.”

JP Morgan also notes that two other risks to the sector’s financial performance – occupancy and property price risks – also appear to be easing.

“Falling occupancy has been a key challenge over the last year. While pressure remains, we believe it has likely bottomed given the non-discretionary nature of the demand and reduced negative media coverage,” the broker stated. “Concerns over the impact of a drop in residential property prices have also receded as asset prices have stabilised and the pandemic has been well managed in Australia.”

The upgrading points to a better year for the listed providers, which have seen their share prices drop 40% or more in 2020.

Regis, Japara and Estia’s share prices have all fallen since listing

Many in the sector will recall that five or six years ago when the big players first listed on the ASX – aged care was touted as a goldmine for investors with Regis listing at 40% above its expected price in 2014. Fast-forward and continued negative media attention, the Royal Commission and finally COVID have all hit hard. But this play for Regis – and the recent activity around Japara where Andrew Sudholz and David di Pilla have both raised their stake – is a reminder that aged care can still be a profitable business. It is worth returning to StewartBrown’s aged care financial performance surveys and taking a look at the performance of the First 25% of operators (Top Quartile). According to their latest data for the June quarter, the top-performing operators still achieved an operating EBITDAR of $13,591 (excluding COVID funding) per bed. In FY19, the First 25% made $15,334.

Bolton Clarke shows providers can make a profit

Going back to our discussion last week about Bolton Clarke, the Not For Profit is another example that aged care can still turn a profit even while meeting a mission.

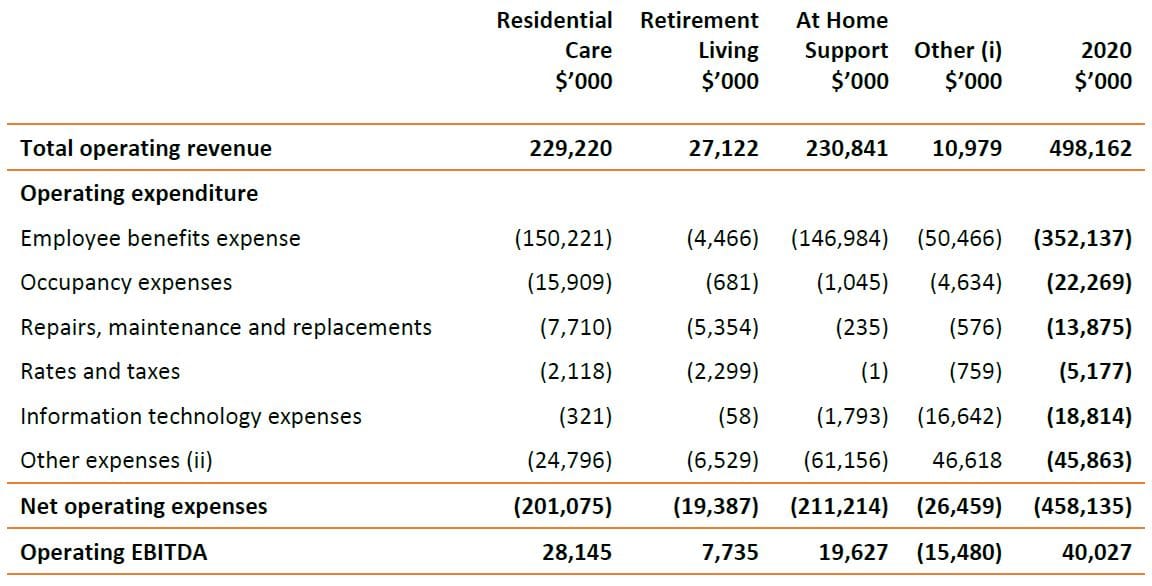

Its annual financial report shows the operator recorded a $28.145 million profit across its 25 aged care homes – that is $1.125 million per home. In contrast, their 25 retirement villages made $7.735 million across 1,935 units – just $309,000. Even with depreciation and amortization of $14.776 million for the aged care homes, that is still a profit of $454,000 per home with many located in regional areas. Consider this too – only 2% of aged care providers have 20 or more facilities according to the latest Aged Care Financing Authority (ACFA) report. 63% of the sector’s 2,700 services are stand-alone facilities while 28% have two to six facilities and 7% have seven to 19 facilities. Having more facilities allows providers to distribute their overheads and staffing costs, saving on cash. While the market appears to be betting on an increase in Government funding to boost the sector’s financial performance, it is clear that scale is required for organisations to be profitable – and this signals that there will be more consolidation to come. Bolton Clarke says it must double in size. As they say, there is no mission without margin – and no excellence or innovation without a margin either.