Top 25 residential providers tighten grip on aged care beds: KPMG

The top 25 residential aged care providers now operate 46.4% of all residential places, up from 44.7% last year, according to KPMG’s 2026 Aged Care Market Analysis.

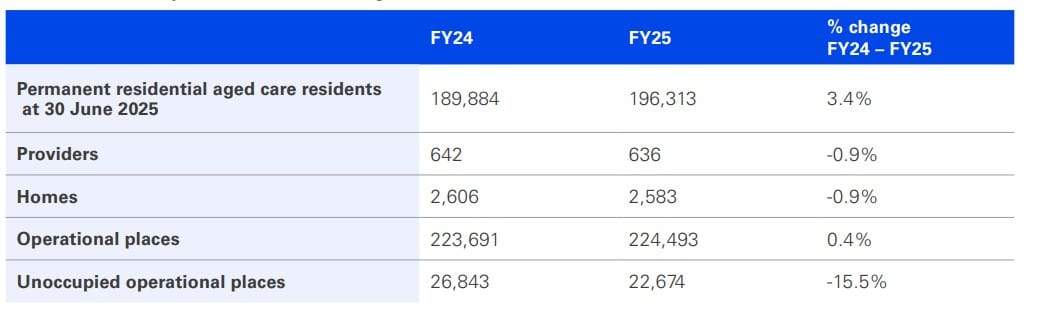

The 18-page report, released today (19 March), reveals that as of 30 June 2025 there were 636 providers, down from 642 a year earlier, while the number of homes also declined slightly. Total operational places increased just 0.4% to 224,493, reflecting limited new development.

That pressure is most evident in occupancy rates, with unoccupied places falling 15.5% and lifting average occupancy to 89.9%. When measured against available beds, the report notes occupancy now sits closer to 94%.

Critically, no new residential providers entered the market during the year.

KPMG attributes this to high construction costs, capital intensity and ongoing delivery challenges, with growth increasingly driven through acquisitions and expansion rather than new builds.

At the top end of the sector, there was no movement in the top 11 providers, with major operators maintaining their dominance. Private providers continue to hold four of the top five positions, while not-for-profits make up 13 of the top 25 by number.

Below this tier, there was more movement, with eight providers improving their ranking. The standout was For Purpose Aged Care Australia – which now operates more than 2,000 beds with a further 900 in development – climbing nine places to enter the top 25.

See the top 25 residential aged care providers below.

Click to view

| FY24 Rank | FY25 Rank | Change | Provider |

|---|---|---|---|

| 1 | 1 | 0 | Opal |

| 2 | 2 | 0 | Bolton Clarke |

| 3 | 3 | 0 | Estia |

| 4 | 4 | 0 | Regis |

| 5 | 5 | 0 | Bupa |

| 6 | 6 | 0 | Uniting Care |

| 7 | 7 | 0 | Calvary |

| 8 | 8 | 0 | Arcare |

| 9 | 9 | 0 | Blue Care |

| 10 | 10 | 0 | BaptistCare |

| 11 | 11 | 0 | Catholic Healthcare |

| 13 | 12 | ▲ 1 | Aegis |

| 17 | 13 | ▲ 4 | Hall & Prior |

| 16 | 14 | ▲ 2 | Mercy Health |

| 15 | 15 | 0 | Anglicare (Sydney) |

| 14 | 16 | ▼ -2 | St Vincent's Care Services |

| 19 | 17 | ▲ 2 | Ozcare |

| 21 | 18 | ▲ 3 | Respect Group |

| 18 | 19 | ▼ -1 | RSL LifeCare Limited |

| 20 | 20 | 0 | IRT |

| 25 | 21 | ▲ 4 | Infinite Care |

| 22 | 22 | 0 | Churches of Christ in Queensland |

| 24 | 23 | ▲ 1 | TLC Aged Care |

| 33 | 24 | ▲ 9 | FP Aged Care Australia Ltd |

| 26 | 25 | ▲ 1 | The Whiddon Group |

The top is no longer moving

KPMG says the lack of movement at the top reflects a maturing market where scale and capital are increasingly difficult to replicate.

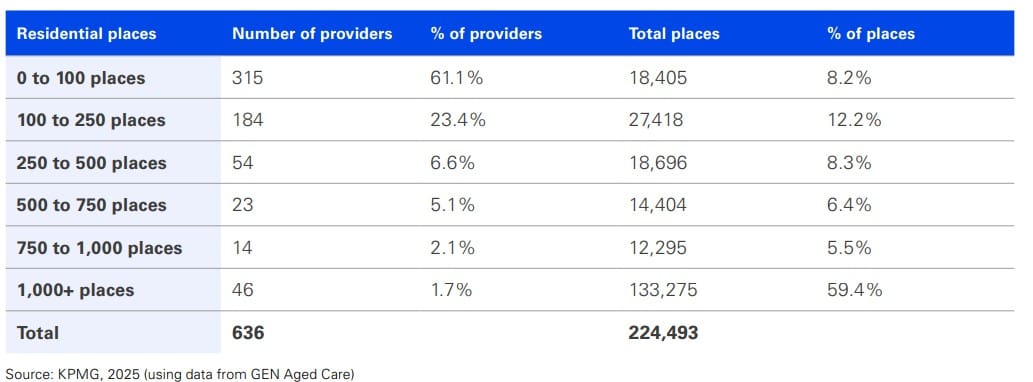

That trend is reinforced by long-term consolidation. Provider numbers have fallen from 807 in FY18 to 636 – a 21% drop – in FY25, while the largest operators have steadily increased their share of places. Today, just 7.2% of providers – those with more than 1,000 beds – control nearly 60% of the market.

By contrast, more than 75% of providers operate fewer than 250 places, accounting for just 20.4% of capacity – see below.

With FY25 seeing significant mergers and acquisitions driven by BaptistCare, Respect and Regis, KPMG expects investor interest to strengthen further in 2026.

“Recent years have seen only a small number of bolt-on acquisitions, but they have helped restore confidence in residential aged care valuations,” Stewart May, Partner, Deals Advisory at KPMG Australia, said.

“Private capital is once again prepared to back scaled platforms, and we expect continued private equity-led consolidation in 2026, particularly in metropolitan areas where it remains cheaper to buy than build.”

But the question remains: will operators be able to meet demand for new beds?

You can download the KPMG report here.