2025 mid-year review: Aged Care & Retirement Living emerging trends

This report highlights the major developments from January to June, focusing on evolving care compliance standards, sector consolidation, and new market entrants and the delayed rollout of the new Aged Care Act and Support at Home Program.

Introduction

Australia’s aged care and retirement living sectors experienced significant transformation in the first half of 2025, driven by landmark Government reforms, increased regulatory scrutiny, and strong market activity, including mergers and acquisitions (M&A). This report highlights the major developments from January to June, focusing on evolving care compliance standards, sector consolidation, and new market entrants and the delayed rollout of the new Aged Care Act and Support at Home Program. It is tailored for banking clients seeking insight into sector dynamics, investment opportunities, and emerging risks.

2025 Sector Review

Key developments, M&A activity and emerging trends

1. Sector consolidation and mergers & acquisitions

Consolidation in aged care and retirement living accelerated in early 2025, driven by regulatory complexity, workforce shortages, and the need for operational scale. Transaction volumes and deal values rose, spurred by strategic growth and distress sales from providers struggling with reforms.

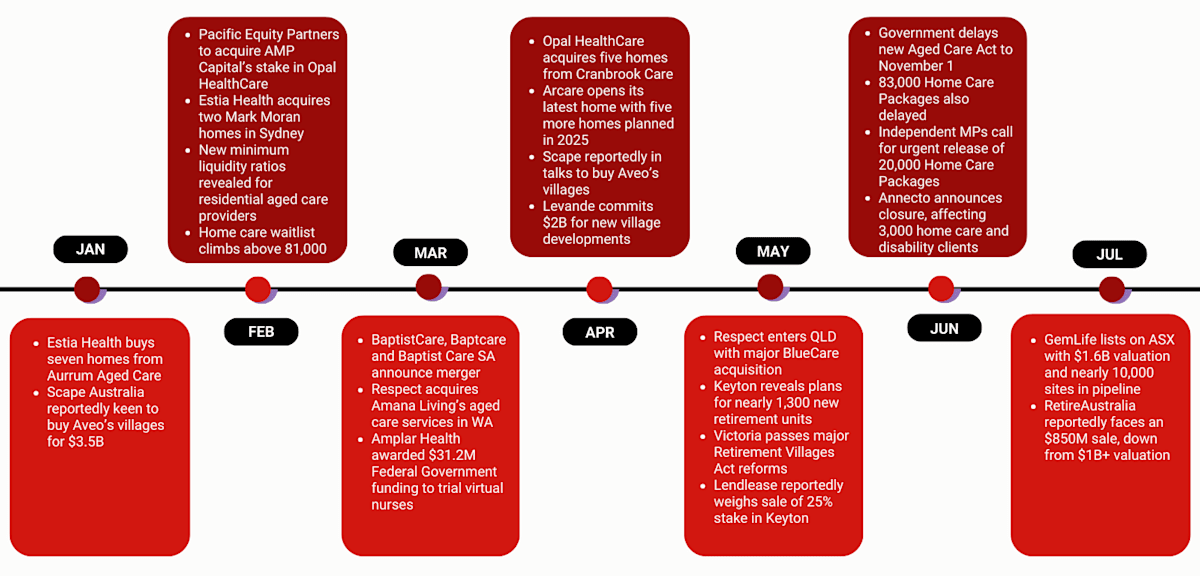

Among the largest transactions, Brookfield Asset Management’s sale of Aveo, Australia’s largest retirement village operator, to Scape Australia’s new seniors living business The Living Company for $3.85 billion will become the country’s biggest direct real estate deal upon completion in July.

Pacific Equity Partners’ acquisition of AMP Capital’s 50% stake in Opal HealthCare – the nation’s largest private residential aged care operator with 133 homes – for an estimated $1 billion strengthened PEP’s market leadership.

The official merger of BaptistCare NSW/ACT/WA with BaptistCare VIC/SA/TAS and Baptist Care SA formed a unified BaptistCare entity, expanding scale, improving care quality, and widening geographic reach, with particular emphasis on retirement living.

“We also continue to see activity in the mid-size space, with operators seeking greater scale. Acquisitions are preferred given acquisition costs per bed are significantly cheaper than build per new beds,” said Belinda Hegarty, Westpac’s National General Manager Healthcare & Professional Services.

2. Industry challenges and emerging trends

Care minute compliance and funding risks

Although care minutes delivered rose 6.5% in Q1 FY25, only 45% of residential aged care providers currently meet mandated care minute targets, risking funding cuts. The Aged Care Quality and Safety Commission (ACQSC) has intensified compliance audits, particularly in metropolitan regions.

From April 2026, non-compliant providers risk reduced Australian National Aged Care Classification (AN-ACC) funding, with assessments based on December 2025 quarter data. Respected aged care accountants StewartBrown forecast tighter margins as providers approach care minute targets amid 2025 Fair Work Commission wage increases.

Delays in the new Aged Care Act compound these financial pressures, limiting reforms that might mitigate ongoing losses in care and accommodation services.

“The pace of change in the sector remains high,” said Belinda. “With mandated care minutes and possible higher staff costs going forward for operators, it’s important that financial forecasts reflect the possible scenarios when engaging the banks.”

Workforce pressures and virtual nursing innovations

Chronic workforce shortages constrain sector growth and care quality. Amplar Health, backed by a $30 million Federal Government grant, will pilot virtual nursing services in 30 aged care homes, assisting clinical decisions, care planning, and protocol management, reducing reliance on scarce onsite nurses.

With a shortfall of approximately 4,000 Registered Nurses in residential aged care – expected to worsen – technological solutions like virtual nursing offer scalable workforce support.

“We are increasingly seeing enquiries for funding to purchase residential properties to house staff, especially in regional and remote areas,” added Belinda.

ICT digital transformation and data integration

The Department of Health, Disability and Ageing is rolling out staged ICT reforms to integrate finance, care management, and regulatory reporting systems. The goal is to reduce administrative burdens and increase transparency.

Operators are encouraged to implement “good, stable systems” for seamless data interchange with Government platforms – enabling improved policy development and public reporting.

3. Retirement living developments

New Victorian Retirement Villages legislation

Announced on 30 May 2025 and due in 2026, new Victorian legislation governs retirement villages, enhancing consumer protections, transparency, and dispute resolution. The law responds to scrutiny over exit fees, contract terms, and living conditions.

Village operators will need to adapt governance and operations, which may impact revenue models but are expected to increase consumer trust.

Market shifts: operators moving from residential care to retirement living

A trend of providers exiting residential aged care to focus on the less regulated, higher-margin retirement living sector continues.

Sydney-based Cranbrook Care sold its five aged care homes to Opal HealthCare in early 2025, citing rising compliance costs and workforce shortages in residential care.

Delivering care within retirement villages

Despite this shift, many village operators are expanding onsite care offerings through internal services or third parties, responding to ageing resident cohorts and demand for care.

Care suites, hubs, and assisted living are increasingly integrated into new developments.

Belinda noted, “This new product challenges operators to align their offerings with resident needs. As the population ages, demand for integrated care within retirement villages will grow.”

5. Financial and investment outlook

Revenue and profitability pressures

Providers face margin pressures from tighter regulations, wage rises, and evolving care standards, balancing quality and sustainability.

Those with scale, operational efficiency, and diversified services are better equipped to manage these challenges.

Investments in automation, technology, and workforce development differentiate resilient providers.

“Investment in innovative technology has been made hard with the challenges of operators over the last five years, however we are increasingly seeing this as a cost included in new builds which will drive efficiencies once in operation,” said Belinda.

Liquidity and prudential standards

In February 2025, the Aged Care Quality and Safety Commission (ACQSC) proposed new financial and prudential standards, initially requiring residential aged care operators with independent living units (ILUs) and retirement village operators to retain 10% of refundable amounts.

Westpac’s submission warned that high liquidity requirements risk diverting funds from essential capital investment during a critical development upswing.

Subsequent sector feedback reduced the liquidity requirement to 2%, with Ageing Australia advising members that strong financial management systems could further ease compliance.

However, heightened liquidity oversight is reshaping providers’ cash flow and capital strategies.

Banks and financiers consider these evolving standards carefully when evaluating creditworthiness and funding requests.

“We continue to monitor this closely as this will have material impacts on operators ability to borrow and will continue to engage with the ACQSC to illustrate the impact on operators’ ability to borrow,” said Belinda.

Major Government legislation and policy shifts

Support at Home Program – a new era for home care (now from 1 November 2025)

The Support at Home Program, initially scheduled to commence on 1 July 2025, aims to replace several fragmented home care programs with a simpler, more transparent model focused on consumer choice and supporting older Australians to live independently longer. However, it also introduces stricter financial reporting and compliance obligations, presenting challenges for providers but opportunities for those able to scale efficiently.

Several local councils, which previously delivered Commonwealth Home Support Program (CHSP) and Home Care Packages (HCPs), have withdrawn from home care delivery ahead of the July deadline, citing rising administrative burdens. Most notably, Annecto, a home care and disability services provider with 3,000 clients across multiple states, announced it would cease operations in July 2025 after 70 years, pointing to shifting service models and financial pressures.

This signals increasing consolidation in home care, with private and Not For Profit providers better positioned to adapt to new regulatory demands.

Delays to the Aged Care Act and Home Care Packages

Despite preparations, the Government announced on 4 June 2025 a delay in the new Aged Care Act’s commencement until 1 November 2025, the first recommendation of the Royal Commission into Aged Care Quality and Safety. The following day, the release of 83,000 Home Care Packages for 2025-26 was also postponed to 1 November – in September, the Government has agreed to release 20,000 new Packages prior to 1 November.

This delay has created uncertainty but also allows providers and investors to refine their transition strategies, particularly around technology to support new systems.

Demand for aged care services remains strong. KPMG’s June 2025 Market Analysis revealed the home care waitlist has grown 125% since mid-2023, while new aged care bed supply has increased only 1% annually since FY18.

“We’re starting to see an uptick in developments again, both in aged care and retirement living,” said Belinda. “Any viable model must put residents first – offering community, care, and flexibility – while remaining commercially sustainable.

“The rising costs of construction have remained the biggest challenges to building new Aged Care beds from our clients. While RVs are able to shadow the property market more closely and achieve market pricing on ILUs, this is more difficult in Aged Care even with the changes in regulated RAD pricing.

“The new developments we are seeing now have different risk profiles from those pre-Covid and more specialised and bespoke solutions are required. Early engagement with banking partners is recommended.”

Harbison fast-tracks dual projects with Westpac’s backing

Harbison, a Not For Profit aged care provider in the NSW Southern Highlands, is breaking new ground – literally – with two major developments set to start later this year: a $32 million Government-backed aged care home in Burradoo and a 35-unit retirement village in Moss Vale.

The retirement village, designed by Independent Design Group and built by North Richmond Constructions, will be the region’s first co-located village – allowing couples to stay together even when one partner needs higher care. With completion slated for 2027, the project aims to meet increasing demand in a “super-aged” community, where transport and access to services are major barriers.

CEO David Cochran says Westpac’s sector expertise and partnership approach have been critical. “We’re a small Not For Profit, and these are big, ambitious projects. They simply wouldn’t happen without a good banking partner,” he said.

Westpac navigated the complexities of blending private finance with a large Government capital grant, ensuring both projects could move forward.

Conclusion

The first half of 2025 was marked by significant change for Australia’s aged care and retirement living sectors. Government reforms, including the Support at Home Program, combined with delayed but forthcoming legislation, continue to redefine the operational environment.

Consolidation is accelerating as large providers seek scale, while new entrants invigorate the land lease and retirement living markets. Providers face ongoing challenges around compliance, workforce shortages, and financial pressures but are turning to virtual nursing and digital automation for solutions.

For banking clients, this evolving sector landscape presents both risk and opportunity. Providers demonstrating scale, operational sophistication, and strategic clarity are attractive financing candidates, especially those embracing innovation and diversification.

Ongoing monitoring of regulatory developments and market dynamics will be essential for informed decision-making and investment.