Will 2026 deliver Australia’s first super-sized aged care operator?

To truly break into super-scale territory, operators will have to build – and this is where the maths starts to fall apart.

If 2025 brought consolidation into the mainstream, 2026 may be the year it reshapes aged care.

For the first time in Australia, the idea of a residential aged care operator with 200-plus homes is no longer theoretical.

As The Weekly SOURCE has reported, M&A activity surged through 2025 as operators repositioned ahead of the new Aged Care Act – some to grow, others to exit while the window remains open.

Rumours continue to swirl that Bain Capital, the private equity owner of Estia Health, has sounded out ASX-listed Regis Healthcare about a merger. At the same time, talk persists that Pacific Equity Partners (PEP) – which owns 50% of Opal HealthCare – has also considered a move on Estia.

Either combination would instantly create the largest residential aged care provider in the country – and push the once-unthinkable 200-home threshold much closer to reality.

Scale is now strategic

On paper, the conditions for further consolidation look ripe.

Occupancy is tightening fast, with residential aged care tipped to be close to full in 2026.

From April 2026, metropolitan operators also face AN-ACC funding penalties if they fail to meet tightening care minute targets. With only around 54% of providers currently compliant, many boards are already reading the tea leaves and seeking to scale or exit.

The limits of buying growth

But here’s the catch: you don’t get to 200 homes by buying alone.

To truly break into super-scale territory, operators will have to build – and this is where the maths starts to fall apart.

The end of the Aged Care Approvals Round (ACAR) on 1 November theoretically gives providers more freedom to decide where, what and how to build.

In reality, the pipeline remains thin. Government forecasts suggest around 1,500 new beds will come online this financial year, rising to 4,000 in 2026-27.

Even if every one of those projects proceeds – and that requires shovels already in the ground – supply will lag demand for years.

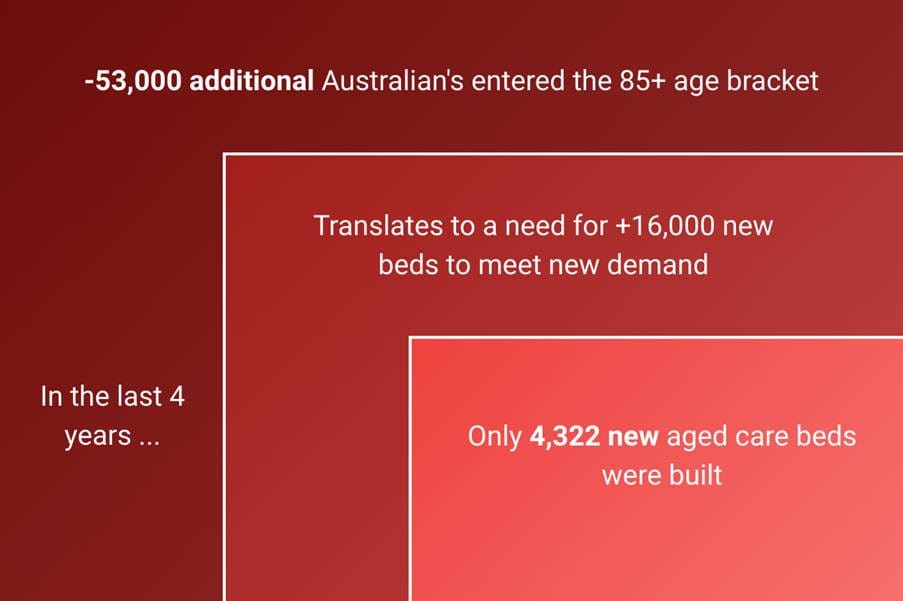

Demand is not the problem

CBRE’s 2026 Seniors Living report estimates that in 2024-25, 32% of Australians aged over 85 – around 168,000 people – were living in residential aged care. By 2030-31, the over-85 population is projected to reach 794,200.

If just 30% of that cohort requires residential care, the system will need around 70,000 additional beds within five years – before even counting younger residents with complex needs.

Home care won’t absorb the gap either. The Mid-Year Economic and Fiscal Outlook (MYEFO) shows funding pressures mounting, not easing.

What ‘super-scale’ really requires

So will 2026 deliver Australia’s first super-sized aged care operator?

Possibly. But if it does, it won’t be because the system suddenly works.

It will be because a small number of operators – backed by the capital and the scale – are prepared to grow in a market where certainty of demand is offset by a continued failure of supply.

There is no single fix. But there are people thinking seriously about it – about capital, integration, workforce, housing and care models that extend beyond today’s silos.

It’s the conversation the sector needs to have – and one we’ll be taking further at the 2026 LEADERS SUMMIT. Register here.