Ansell Strategic forecasts more aged care “acquisition opportunities” in next 12 months and shows Top 25 Quartile Not For Profits make biggest ‘surpluses’

You can download the full report HERE

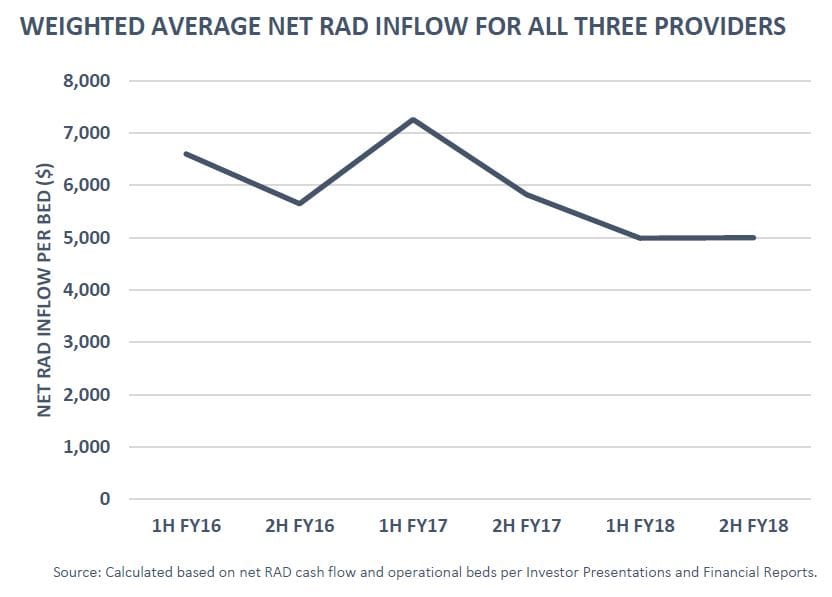

The increased cost of the Government’s new “heavy-handed” care compliance regime is good news for the listed providers, according to their latest ‘In a Nutshell’ report on their performance. Smaller operators will struggle to survive. “Like Japara’s Riviera acquisition, these activities involve distressed assets that sell for much less than historic purchases but carry substantial compliance risk. Larger operators like the listed providers are better equipped to manage the heavy turnaround investment required to mitigate this risk.” The new aged care standards due to start 1 July 2019 will also create further acquisition opportunities next year according to the aged care provider advisers. Their report notes that the big three’s EBITDA per bed per annum results have declined or remained steady since FY16 and apart from Regis, these results have continued to sit below the top quartile performers recorded by StewartBrown. Their research shows the top quartile EBITDA was $18,300 in FY17 – for the year to date, it’s dropped to $17,600. In contrast, Regis has fallen from $20,100 in FY16 to $18,200 in FY18, while Estia has declined from $18,800 to $15,000 over the same period. Japara is also well below the top quartile, with an EBITDA per bed of $12,000 in FY18. Staff costs are also expected to stay the same or increase with the new aged care standards. The results are a contrast to the Australian Nursing & Midwifery Foundation’s recent scare campaign against for-profit aged care providers, which resulted in a Senate Inquiry into their financial and tax practices due to report next week on 20 September. Ansell says these results are likely to be further impacted by the increase in the number of supported residents. As we covered here last week, more residents are now choosing to pay a Daily Accommodation Payment (DAP) than a Refundable Accommodation Deposit (RAD) – a 19% increase in metropolitan homes. In FY18, Regis’ average incoming RADs have only increased by 3% – for Estia, it’s 5% while Japara has had a decline. Ansell predicts that net RAD inflows will continue to slow thanks to a range of factors:

- New residents are now replacing those who entered under the 2014 reforms that allowed aged operators to charge RADs for residents previously ineligible to pay lump sums – resulting in a dramatic increase in funds.

- The number of supported residents has also increased in recent years, paying either DAPs, combination RADs and DAPs and government-subsidised residents.

- The new supply of aged care facilities has led to a greater competition for beds, leading many providers to lower their pricing to maintain occupancy.

- RADs are also closely linked with house prices, which have slowed significantly (see our housing story above).

They add that many of their clients now prefer DAP payments to finance new developments. “The DAP represents a return of just under 6% of what would have been paid on the RAD (and increases in line with interest rates). Because the RAD is normally well above the cost of construction per bed of the home, this usually represents a strong return on investment.” The question is now: will this prove attractive enough for the big funds to consider moving into the sector?

You can download the full report