Has the retirement village sector lost its mojo? Just 2,300 new homes a year being built

Across the three years from 2017 to 2019, just 6,872 new village homes entered the market, or 2,290 a year. This means that the village sector is going backwards in market penetration. To maintain the baseline 6% the sector regards as a standard (...

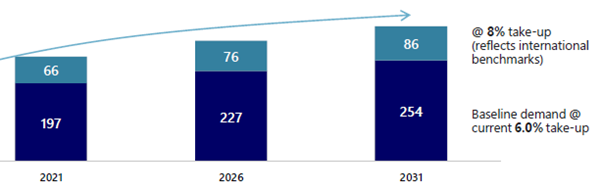

Across the three years from 2017 to 2019, just 6,872 new village homes entered the market, or 2,290 a year. This means that the village sector is going backwards in market penetration. To maintain the baseline 6% the sector regards as a standard (a pre GFC benchmark), around 5,500 new homes need to be built and delivered. We analysed the new villages to be listed on our web portal villages.com.au across this period and it revealed the stats above. Just 77 village operators (average 26 a year) out of 800 committed to develop a new village. 17 were new operators to the sector (or six a year). Across the three years, three operators delivered two new villages, and one delivered four new villages. Therefore 67 villages were one-off commitments. Further questioning the commitment, or reflecting the direction of the consumer market towards smaller villages, just 23 villages were sized at 100 homes or larger. The chart below is from Stockland’s HY20 Investor Presentation, highlighting the new construction – and operator commitment to investment – that is required to maintain 6% baseline growth the sector talks about. It will require over the next five years another 30,000 village homes – or 6,000 a year. At an average investment of say $350,000, this will require $10.5 billion in funding ($2.1 billion a year). We don’t see the appetite for this at present.

This is a crazy situation. Let’s consider a couple of facts:

- The village model delivers proven and unrivalled resident satisfaction because it delivers a service that is greatly valued by residents/customers.

- A healthy portion of village operators are building and selling what they build, and fast.

- Just 22,000 village homes come on the market each year, yet our DCM Research reveals there are 79,900 customers actively considering a village purchase today. Demand does exceed supply.

- Our research, the performance of innovators like LDK, Ryman and Australian Unity, and the Aged Care Royal Commission each demonstrate there are evolving village models that appeal to today and tomorrow’s customers.

- And finally, New Zealand’s village population was at 6% penetration in 2006 – it’s now close to 14%, with a slight variation in their model.

What conclusions can be drawn? It’s simple really; if a sector or a business is shrinking, it is dying. We need to be taking advantage of the strong base that exists and learn from the operators that are doing so well by offering new value propositions. The numbers are compelling; positively if we regain our mojo, and negatively if we don’t.