Prediction: The retirement village business model will be very different five years from now

Customers will design the future village model, not operators. All resident contracts will need to be rewritten to keep villages viable as care becomes a cornerstone of the value proposition.

It is already happening. The village business model is being changed from within, with residents coming in with higher levels of acuity, and staying longer.

Longer stays hit revenue

One of the largest operators admitted last week that they are looking at 10 and 11 years average occupancy compared to nine, which means their near term sales and revenue is being cut by up to 40% as they wait for their DMF turnover, and there is little they can do about it.

The lawyers around the country are telling us that residents and their families are refusing to move out of the village to go to residential aged care (if a bed is available), and again, there is nothing the operator can do about it.

To back this up, the 1 May (2026) Victorian legislation changes now prohibit a resident’s occupancy being challenged if home care is suitable and available.

From independence to dependency

Village operators now talk of 30% of residents being reliant on home care services. When does a retirement village shift from ‘independent’ living to ‘dependent’ living and the operator having a duty of care to the resident to provide staffing to match?

Think of the new normal being 10 staff for 100 residents. The customer will not only demanding support but also wellness as an offset to the negatives of ageing.

Rising costs and contract reform

We predict within three years – 2029 – this will be the case, demanded by real people residing on your property. And your business model will collapse as expenses exceed income.

Given residents will be in place for even two years more than average – 11 years – you will have to rewrite existing contract to capture cash now to cover costs.

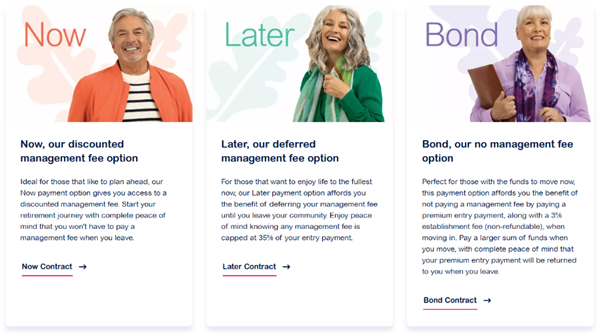

Private village operator Aveo is an early leader. It already has 30% of its contracts now featuring the DMF paid upfront. Not For Profit operator Anglicare is matching this percentage.

Equally, the resident, your customer, will be asking you to rework the contract to give them access to their equity to pay for private home support services as government funding falls behind demand. They will also be topping up Government Support at Home packages (which will be fewer and less generous).

A more complex financial model

The financial model for villages will get correspondingly far more complex. You will need new systems. Additional services will have to be accounted for, new sources of revenue will come with regulatory strings. Current village regulations via the Retirement Village Acts, will not keep pace, complicating things further.

As the operator, you will also be looking for efficiencies through technology. You will have a big physical campus with frail and ill people in dispersed homes; how will you responsibly and efficiently keep connected to them without tech?

Higher prices and selective entry

Given this additional expense but balanced by increased demand (given no aged care beds and the alternative of isolation in the family home), village operators will be able to demand higher prices, stronger contract terms and be selective on who you accept as new residents. But it will take nerve and marketing to bring the customer along on this journey.

And this is where we predict the Community Apartment Projects (CAPs) competitor will emerge and steal the cream of the village customers.

CAPs are strata developments that add a slick care support overlay to their offering. A concierge service, 9C construction to age in place, tech to partner with Hospital in the Home services like St. Vincent’s, Silverchain or Amplar Health.

A new style of strata management will deliver these CAPs with a brand of trust, but at a price. It is already happening with property developer Platino in Sydney with its Jardin project, complete with care suites being built into their apartment development, and Melbourne developer Tim Gurner is travelling down the same path.

CAPs offer strata ownership with full capital gains and no DMF. Village style strata management is an additional fee. The more wealth customer has, the more attractive this proposition is, eating into the traditional village market.

Veteran developer David Devine has 626 apartments in his second CAPs project at Southport (QLD).

Both villages and CAPs operators will be seeking partnerships with clinical care providers, seeking their scarce workforce plus their virtual health tech. This will be a race to sign partnerships first because demand will exceed supply, and if you are not partnered, life will be very difficult.

We see all the points above already coming to life across the country, led by the customer – seeking out villages as a safe haven from residential care, staying longer with high acuity, expecting more from operators, developing a voice.

Where are you in this five year journey?

Not a member and want to keep reading SATURDAY? Click here to access the 30 day free trial.