Residential aged care: same, same but profitably different

The business of residential aged care will change over the next five years, but not markedly except it will stop losing money each day on each bed – it will be profitable.

While Federal Health and Aged Care Minister Mark Butler openly states that we need to build a new aged care home every three days for 20 years, he and we know that will not happen.

The 5,000 bed funding in this budget will take five plus years to deliver if operators can be found to take them up.

In fact, relatively speaking, virtually no new homes or beds will be delivered within the next five years or the next 10 years, if ever.

Demand drives pricing

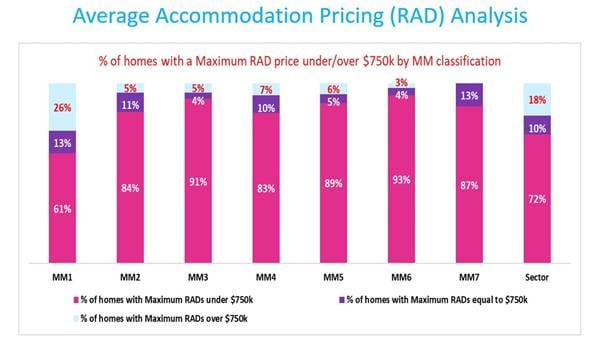

Historically, providers have not charged the prices that they could for accommodation – see the below slide from StewartBrown. Approaching 90% of homes do not reach the $750,000 RAD they can charge without Government approval except in metro markets where even they have 61% reluctant to go hard on RAD pricing.

But operators now have a monopoly on current and future supply of beds at a time of ballooning demand. History says they will be in a position to increase prices and take opportunities to maximise returns on their investments, and they will.

The sheer number of real people desperately needing a bed and the fact they are the Baby Boomer generation with home equity means operators will be able to play hard – and they already are.

High cost or low value customers are being declined by residential care operators now, which is why 3,300 people languish in hospitals plus many more at home are languishing alone with only family support (if they are lucky).

Rising accommodation costs

Daily Accommodation Payments (DAPs) will grow, making RACs more viable. The argument, particularly in country regions, that family homes are not up to the value of $1 million Refundable Accommodation Deposits (RADs) in the city is reasonable. But desperate people will find the cash for 10 to 12 months in a RAC because finance products are already being planned to fund this demand.

It may be the Government, as it is New Zealand, that provides a low interest loan with security over the home (a product already available in Australia but not utilised by the sector).

Private aged care expands

As the demand rapidly grows, some operators will walk away from Government funding and offer 100% private aged care. This is viable now, with some RAC operators telling us that they are down to 10 months average RAC occupancy (from the traditional 2.2 years just two years ago).

If this is the case, as a private pay customer at say $750 a day over 10 months, the cost would be $228,000. In a metro area, with a RAD of $1 million, and additional services of say $80 a day and co-contribution requirements, the $228,000 will likely be around $120,000 over what they would pay under the Government/public system. If it guarantees a bed and a dignified end of life, then some, if not many, people will pay it.

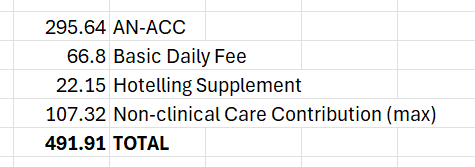

Here is the latest IHACPA recommended pricing structure:

Pressure on Government

Those larger operators that stay within the Government system will flex their demand/supply muscle and coerce the Government to let them make a market profit. The lever is likely to be refurbishments.

Across the country, the majority of RACs are 25-plus years old. Old hands say they need to be refurbished every 15 years to remain economically viable. As public outrage increases around lack of beds, operators are in the box seat to renegotiate the current Government-led concept that operators are a utility that should not make profits beyond utility profits of ~4%.

Reinvesting in old buildings doesn’t stack up at a 4% profit level (and even lower yield).

The alternative is a continued policy of cherry-picking RAC customers, resulting in more people in hospital beds. The Government will relent and allow increased charges to the customer.

New operating models

In rural areas, co-operatives are emerging, where back office services are centrally provided. Apollo Care and Respect are leading this evolution, and it can apply to all RAC operators, including metro. This will deliver lower costs and higher net returns (profit).

The acceptance of virtual nurses and virtual health to a high clinical level will also introduce efficiencies within the next three to five years, making RACs more viable. Virtual health and AI diagnosis will break the Registered Nurse hurdle to expanding services as well.

AI-related redundancies in the broader community will release people willing to work in residential aged care, solving the workforce challenge.

Dementia remains unresolved

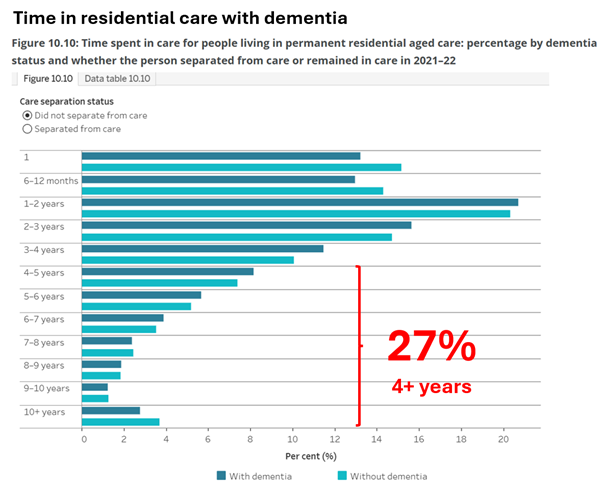

The only dark space on the horizon is dementia, where RAC occupancy is traditionally two years but historically 27% stay four years or longer. Approximately 50% of RAC residents display a level of cognitive decline.

These residents are not working now as an economical customer and will not in the future for aged care homes looking to maximise income to cover their narrow profit (and therefore sustainability) margins.

The solution is unresolved. The condition does not require the clinical levels of a RAC for much of its condition so when RAC bed supply is extremely limited, it is not productive to accommodate a resident with dementia, and nor is it the optimum environment for the resident.

Alternative dementia care

Two solutions are on the table.

Memory units, either stand-alone or as an offshoot of a traditional RAC makes sense, but the funding and the red tape regulations need to be loosened from the traditional RAC to make them viable. (For instance, the 215 minutes of registered nursing may not be required).

The alternative is increased resources and technology to support the person in their own home, a strategy that HammondCare champions. Rather than two-plus years in a traditional RAC, this may be pared back to six months.

The funding needs to be shaped to these two options such that they are viable – it is inevitable.

A more viable future

On the above analysis, residential aged care is projected to move to profitability across the board but the investability to support large scale new bed construction is unlikely due to the grip of Government on regulations and customers preferring new options if they are going to be paying a high price.

At this time, traditional RAC operators are transferring to the low regulation/higher pricing retirement village model, and this will continue. But they will not deliver the quantity of new accommodation that demand requires.

The residential aged care business model will remain largely unchanged, but more viable.

Not a member and want to keep reading SATURDAY? Click here to access the 30 day free trial.