Residential occupancy drops to 86.5% for For Profit providers, latest ACFA report reveals – providers with two to six homes the worst performers

In October last year, the Chair of the Aged Care Financing Authority (ACFA), Mike Callaghan AM PSM and former Chief of Staff to Treasurer Peter Costello – gave evidence to the Senate that the sector may not be financially sustainable – eight...

In October last year, the Chair of the Aged Care Financing Authority (ACFA), Mike Callaghan AM PSM and former Chief of Staff to Treasurer Peter Costello – gave evidence to the Senate that the sector may not be financially sustainable – eight months on, ACFA has released its Eighth Report on the Funding and Financing of the Aged Care Sector and the news is even grimmer. In total, the sector made just $264 million profit in 2018-19, a 39% drop from the $435 million recorded the previous year. On say $15 billion turnover for the sector, this is just 1.65%.

National occupancy dipping below 90%

The 174-page report – which was compiled using providers’ 2018-18 financial reports and feedback from consultation conducted in early 2020 prior to the coronavirus pandemic – reports that residential occupancy has dropped to just 89.4%, down from 90.3% in 2017-18 and 91.8% in 2016-17. Check out the breakdown above. As you can see, Not For Profits has the highest occupancy rate at 91.5%, followed by Government-run providers at 90.4% and For Profits sitting behind at 86.5%.

For Profits at a disadvantage

Older facilities recorded the biggest falls in occupancy, according to the report, reflecting their lower appeal to consumers compared to new or refurbished homes. It is worth noting that For Profit are concentrated metropolitan areas with Mum and Dad owners, and who don’t have balance sheets the banks will support for major refurbishments. 89% is the break-even point for providers, according to Health Metrics CEO Steven Strange – suggesting more than half of providers don’t have the resident numbers to make a profit. Remember too – these numbers are from before the impact of COVID-19 when many providers reported experiencing further declines.

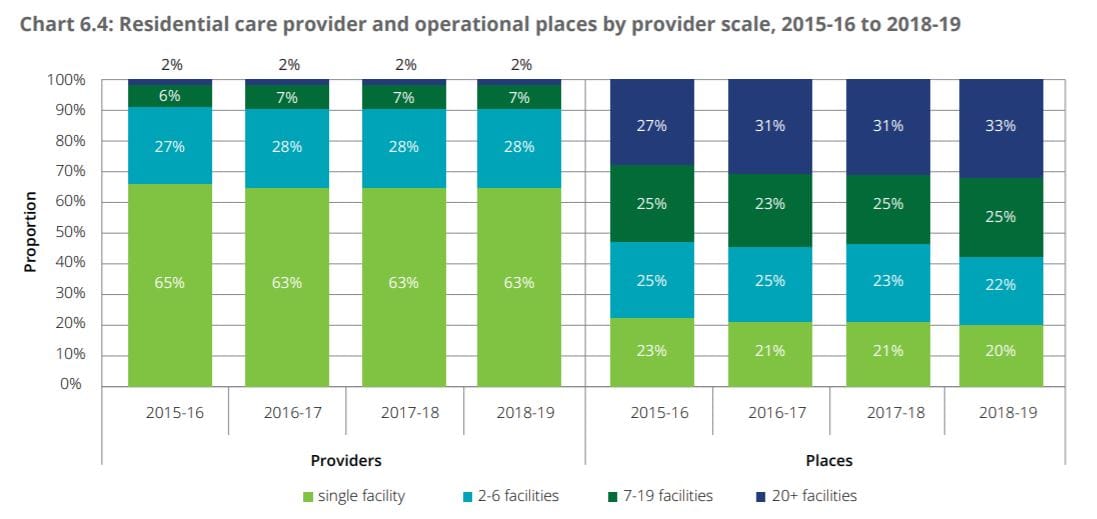

Single facility providers the best performers

ACFA reports too that the financial performance of providers held steady in 2018-19, compared to the previous financial year. The average Earnings Before Interest, Tax and Depreciation (EBITDA) per resident for residential care providers was $8,523 in 2018-19, a 2.5% decrease from $8,746 in 2017-18 where there was a 24% fall from $11,481 in 2016-17. Scale did play a role. Single facility providers – which account for 63% of all providers – were the best performers, with an average EBITDA of $8,907 in 2018-19, up from $7,110 in 2017-18.

Providers with 20 or more facilities – which comprise only 2% of providers – were the next best with EBITDA per resident of $8,861, but this was a considerable drop from $10,622 in 2017-18.

Providers with two to six homes the worst off

However, providers with between two and six facilities (28% of the market) were the worst performers for the third year in a row, recording an average EBITDA per resident of $7,212, though this was an increase from $6,340 in 2017-18. Overall, 42% of providers still reported a loss in 2018-19. ACFA adds that without the additional $320 million paid to providers through the one-off 9.5% subsidy increase between March and June 2019, 48% of providers would have reported a loss and the average EBITDA would have declined to about $7,000, or a 20% decline on 2017-18. Feedback from their consultation this year also showed providers’ financial performance continued to deteriorate into 2019-20 with little or no growth in ACFI revenue.

Home care providers restructuring to make a profit

Home care providers also saw little improvement in their results in 2019-20 with financial returns flat, despite the increase in the number of new packages being released. Those that did see a lift reported that this had only resulted following a significant restructuring of their business model, targeted advertising and recruiting new staff – in short, they spent money to make money. The report also noted the increasing shift to DAPs and its financial implications, not only in how providers run their business but also in relation to COVID-19. “A significant potential risk for providers is a sizeable and quick cash outflow in repaying RADs in response to the spread of COVID-19 in a facility. In such a situation, new residents may not be replacing departing residents. In addition, a downturn in the housing market as a consequence of COVID-19 would flow through to lower use and lower value of RADs,” it states.

Question mark over future of RADs

Interestingly, ACFA notes that the Aged Care Minister, Senator Richard Colbeck, has asked the body to undertake an analysis on the future role of RADs in the aged care market which is scheduled to be completed in 2020 or early 2021. In addition, ACFA says there is “strong interest” from providers in lifting their revenue through additional services with some introducing a ‘menu’ of additional services for a fee. However, others said while they were keen to do so, they had not because of the regulatory uncertainty over which services could attract a fee – think Bupa’s $6 million penalty by the ACCC.

Sector in an unsustainable position

ACFA concludes that COVID-19 has arrived on top of a steady three-year deterioration in providers’ financial position. “This is not a sustainable position if the aged care industry is to meet the needs of an ageing society,” they state. With the delay in the Royal Commission hearings putting off when the Government can respond to its recommendations, ACFA recommends a number of measures in the interim to deal with the underlying financial pressures in the sector, including:

- Meeting the conditions for uncapping the supply of aged care services as outlined in David Tune’s 2017 Legislated Review of the Aged Care Act, namely the Government needs to understand the underlying demand; consumers making contributions to the cost of care; a robust system for assessing eligibility for and the equitable supply of services across population groups.

- Establishing an ‘efficient’ price for aged care services to avoid “over generous support” for inefficient providers while allowing a sufficient return for efficient providers so they will invest in the industry.

Government must balance aged care with other spending priorities

However, they also acknowledge that the Government can’t ignore “fiscal realities”. “Prior to the impact of COVID-19, a focus of the Government was on ensuring that its expenditure on aged care was balanced against other spending priorities and was consistent with the sustainability of the Government’s overall fiscal position. That balancing task will remain after the COVID-19 crisis, albeit in more difficult circumstances.”