All but Victoria village sales ‘alive’ – but this is short term without following the basics

Around 25% of operators are always selling well, by following the basics, again reiterated by our research. For instance, yesterday I got an SMS from Paul Browne, Managing Director at LDK Seniors Living, saying his October sales at his one new...

Last Thursday I was in Adelaide. Our DCM Institute team had come together from three states to review our 2021 professional development program for village management – some of us flew and some had to drive to get there (3,000km round trip). Anyway, the resounding message was the positive atmosphere across the retirement and land lease sectors, with real sales taking place across all states except Victoria.

COVID driving sales – 43% vulnerable

Our team had spoken to over 150 villages in the past month and almost universally the feeling has been upbeat. The pipeline of prospective buyers has been steady and they are ‘walking down the drive’ feeling educated and ready to make decisions. Instead of one in three being a buyer, talk is of one in two, with the children also being positive in their support. The reason: COVID. Prospective buyers are apparently seriously seeking a ‘safe harbour’. Anecdotally, this is verified by both the older age of buyers and the fact that studio, one-bedroom and serviced apartments are ‘walking out the door’. This is great news and verifies the early results from our DCM Research project conducted with Australia Online Research (AOR) from March through to July. It identified that 43% of all people aged 60+ felt an increased sense of vulnerability as a result of COVID. 20% are now concerned about the suitability of their home.

Is sales confidence sustainable?

We are optimists and so would like to think these new sales levels are sustainable. But we also lived through the Global Financial Crisis (GFC), witnessing that sales can stall for up to three years. After an initial positive action, loss of confidence settled in and sales basically stopped. Will this happen again? People have to sell their homes to buy. At the moment property values are holding up, but is it confidence that is holding it up or fewer properties being marketed. The CoreLogic chart above indicates the latter – fewer properties are being marketed, by about half outside of Sydney. And you have to ask why. The table shows auction numbers for last week (26 October) compared to the same week last year. Ignoring Melbourne given the lockdown, Brisbane, Adelaide and Perth had half the properties offered for sale. This means that people are holding back and/or didn’t have confidence in demand enough to go to auction. If our economy stumbles after the Government supports are withdrawn, even fewer properties will be offered, and buyers will be fewer. First home buyer grants are capped and expire 30 June next year. It is possible, even likely, that, once the fear of COVID (and vulnerability) subsides, the urgency of selling the family home and buying into a village could subside.

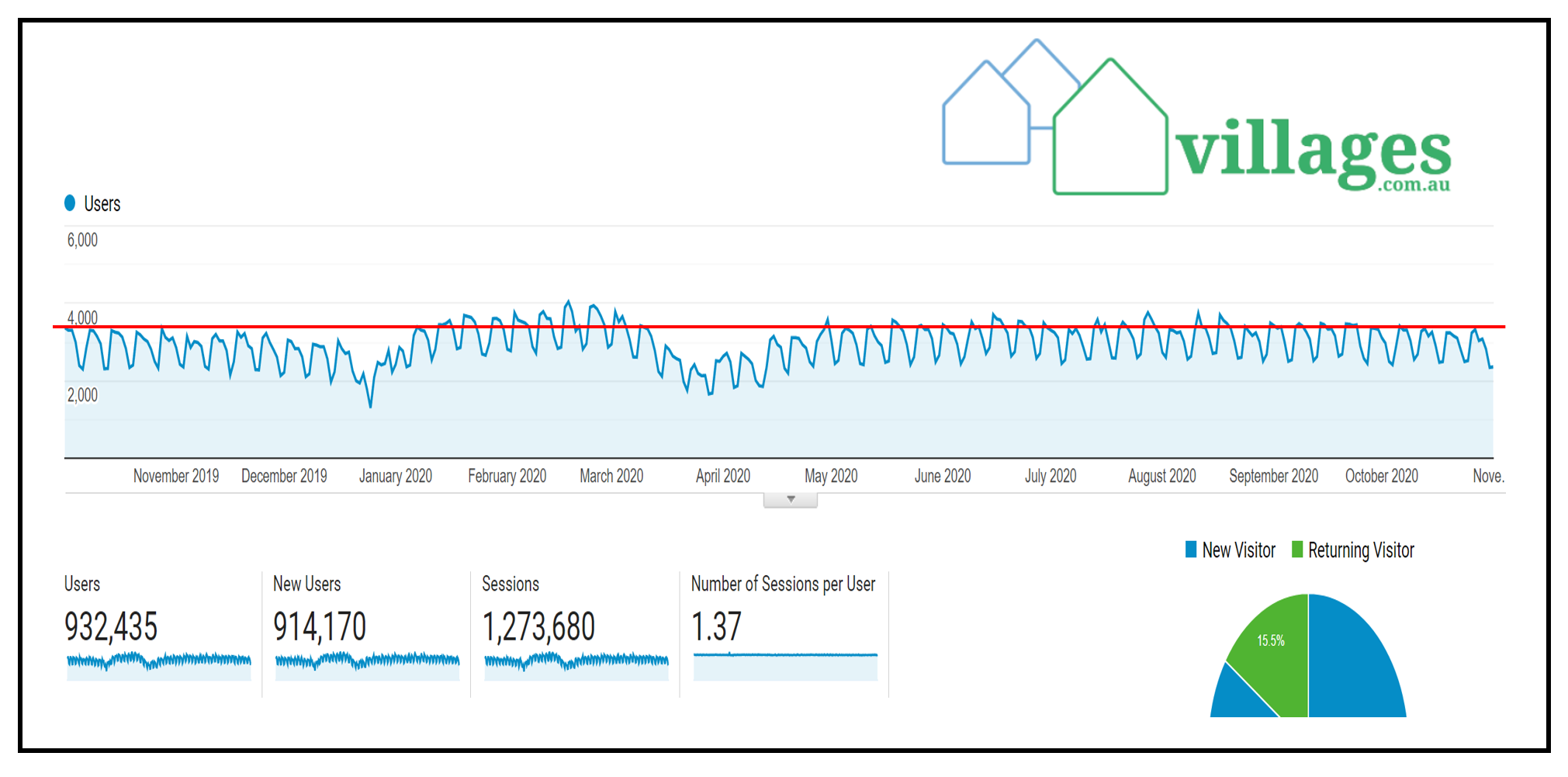

Village demand has always exceeded supply

Our research and experience, year in and year out, is that demand for the village solution far exceeds supply. See the village enquiry in the chart above. Over 900,000 people searched for a village in 12 months. Only weak marketing holds village sales back. Irrespective of COVID, a minimum of 3% of all older people are ‘actively interested’ in buying into a village. In raw numbers, that’s 72,100 people today. Only 22,200 village homes are available each year to sell. Our DCM Research shows the potential is 18% of people all up, divided between these cohorts.

Around 25% of operators are always selling well, by following the basics, again reiterated by our research. For instance, yesterday I got an SMS from Paul Browne, Managing Director at LDK Seniors Living, saying his October sales at his one new village in Canberra was 21 homes. (See the next story). At times we underestimate what villages deliver residents. We shouldn’t. There is a reason why over 80 people move into a village home every day of the year. It is security, it is community, it is confidence that support is built in. Villages are a step up, not a step down. Village marketers must stay focused on the basics for success – resident outcomes. COVID is a short-term bonus.