Govt report exposes home care margin squeeze

- Care management: Fees previously cross-subsidised loss-making home care services

- Support at Home: Providers likely need higher service prices

- Home care earnings: EBITDA rose strongly during 2024-25

- Profitability warning: Early Support at Home margins deteriorating

A Government report on the Australian aged care sector has reinforced the case for higher prices under Support at Home if operators are to maintain margins.

The Federal Government’s Financial Report on the Australian Aged Care Sector 2024-25 shows the cost of delivering care management in 2024-25 was 9.6% of total home care income.

In contrast, income from care management fees was 17.3% of total income for the sector.

“These results indicate that providers may be using margins on care management services to cross-subsidise losses in other services,” states the 121-page report.

The findings echo those made in previous Government reports.

Yet, the findings reflect the period before the 1 November 2025 rollout of Support at Home, which introduces caps on care management of 10% of package income.

Going forward, the Financial Report states providers will have to “price all services reasonably” – in other words, operators will have to charge higher prices to offset the loss of care management income under Support at Home if they are to maintain margins.

Earnings

The Financial Report also provide a general snapshot of the sector with home care EBITDA margins firm in 2024-25.

At the sector level, they rose 0.5 percentage points (pp) to 6.9%, up from 6.4% in 2023-24.

Home care sector earnings also rose strongly.

At a sector level, Earnings Before Interest Tax, Depreciation and Amortisation (EBITDA) rose 27.7% to $607.7 million, up from $476.1 million in 2023-24.

The result was equivalent to $5.91 per care recipient per day (pcrpd), a 21.2% increased from the $4.88 pcrpd achieved in 2023-24.

Earning growth was driven by:

- a 5.3% increase in claim entitlement days from 2023-24 to 2024-25, reflecting an increase in the number of Home Care Packages allocated by the Government;

- a 3.7 pp increase in the proportion of Home Care Packages used by each recipient from 82.7% in 2023-24 to 86.4% in 2024-25; and

- the 3.1% increase in the home care subsidy from 1 July 2024.

Despite the broadly positive home care earnings report, StewartBrown’s 1H 2025-26 Aged Care Financial Performance Survey Sector Report indicates “there are signs” Support at Home, which commenced after the period of this report, is “less profitable” for providers.

StewartBrown, with a sample of 86,324 home care packages or 29% of the sector, showed operating margins showed a “significant” decline in 1H 2025-26 which deteriorated particularly strongly in the December quarter – after Support at Home came in.

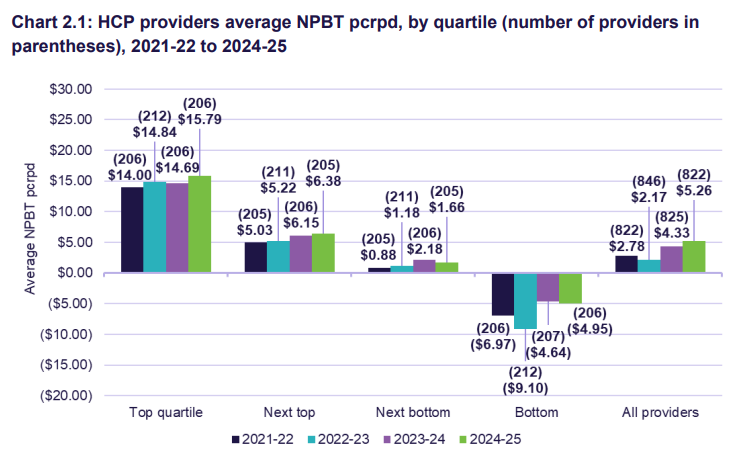

Profitability varied significantly across the home care sector

The Financial Report showed providers in the top quartile recorded a notable improvement in Net Profit Before Tax (NPBT) in 2024-25, however the bottom two quartiles recorded weaker results – see chart below.

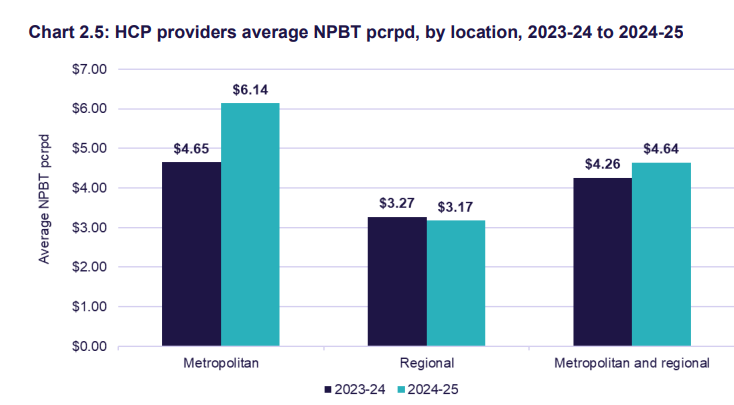

In 2024-25, average NPBT results improved for metropolitan providers, while for regional providers, NPBT was broadly steady – see below.

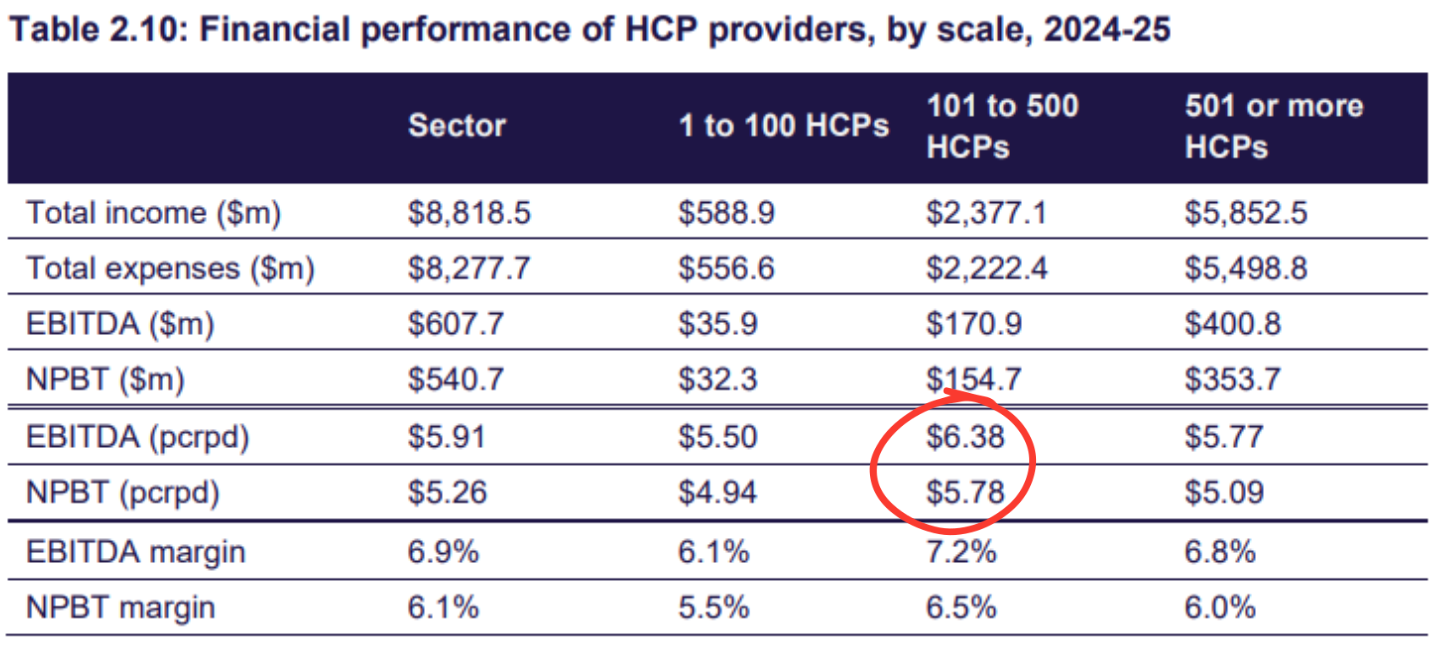

Home care providers servicing between 101 to 500 Home Care Packages reported the highest earnings pcrpd – see below.

Other notable findings

- The median length of time accessing home care services rose 13% to to 23.0 months in 2024-25, up from 20.4 months in 2023-24.

- Unspent funds rose $0.5 billion over the year to $4.1 billion as of 30 June 2025.

- The proportion of providers reporting a positive NPBT was 73.0%, steady with 2023-24.

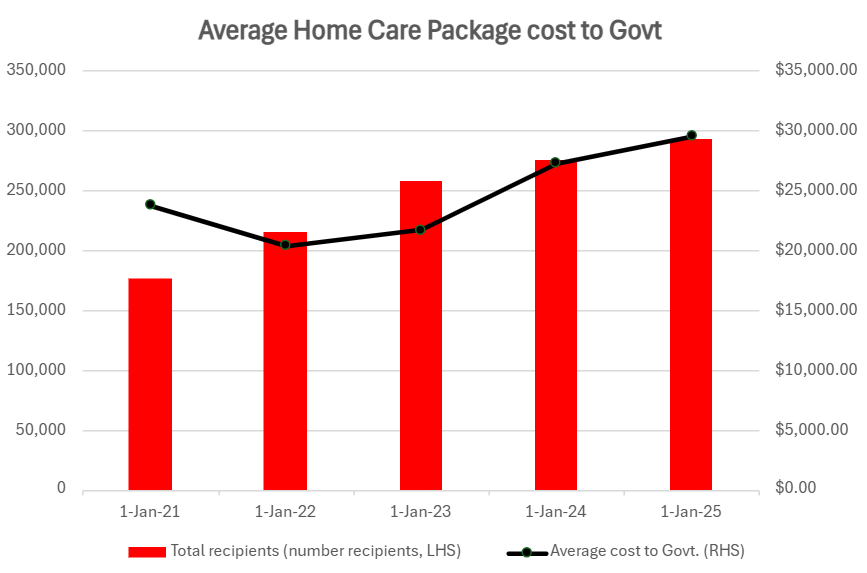

- The average Govt cost per Home Care Package was nearly $30,000 – see below.

StewartBrown’s survey said the earnings they saw in their 1H 2025-26 survey were “not sustainable”.

Watch this space.